The GRIT 2017 Q3-Q4 Report is now available for download at GreenBook, and below you can find one of the key sections: the Challenges & Opportunities for the industry. Jon Puleston of Lightspeed, with contributions from Ryan Soulet of the MSU MMR program and Tom Anderson of OdinText, led the charge in analyzing thousands of verbatim responses to the questions we asked about challenges, solutions, and opportunities for the industry in the year ahead. This gives us a quick read on where the “heads and hearts” of researchers are and offers a glimpse of where the industry may be going. This blog first appeared on the GreenBook blog as part of their GRIT Sneak Peek.

Opportunities & Challenges

To understand what Challenges and Opportunities exist in the research industry today, we asked various open-ended questions to provide research professionals the opportunity to state their viewpoints.

CHALLENGES

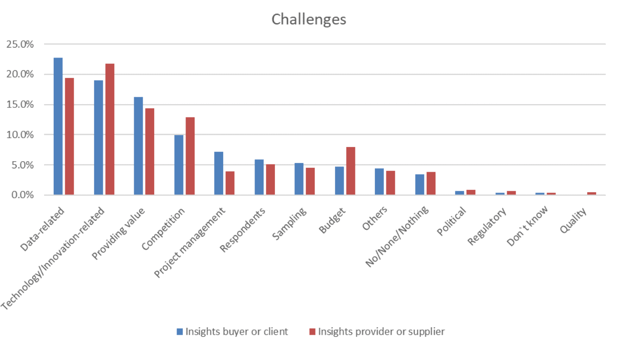

Data related challenges

Analysing the open ended feedback concerning challenges facing market research and suggested solutions you can see from the chart above that a great majority of the comments, nearly 1/3rd of the feedback, are to do with data. The industry is awash with data right now and with it comes all sorts of challenges: what do with it, how to analyse it, finding the skills to analyse it, how to compete in a new data rich research market place.

This “data challenge” can perhaps best be summed up in three key themes:

- Technological/Innovation-Related: Continuing to adapt to the speed at which technology is growing and learning how to utilize/integrate its capabilities to provide businesses with better results.

- Data-related/Providing value: Becoming more than just insights providers but partners with businesses in research endeavors by truly understanding the greater purpose of their research such that we are change activists who provide compelling stories.

- Competition: How to handle the increased presence of cheaper online DIY research tools and the encroachment by non-research based companies into our market.

Respondents expressed growth in technology/innovation (21%) as the biggest challenge facing the industry. As new technological advances and methodologies continue to become prominent, so must the industries understanding of how to leverage them. Technology presents great advantages for collecting data but isn’t widely accepted by the industry as a whole and often comes with price constraints. Additionally, supplier side researchers will have to act as salesmen to convince organizations that investment in new research technology is valuable. The challenge is how do we innovate while maintaining quality standards and statistical validity? Especially as there is growing threat of non-traditional research companies (Tech/consultant companies) that will continue to gain market share if traditional market research suppliers don’t continue to evolve, as expressed by the quote below.

“Tech companies, while not market researchers, know how to leverage technology to reach consumers and deliver a new differentiated offers. Traditional MR companies are stuck in the past with being too purist, too reactive, and too slow. Google and Faceboook can all provide access to the consumer free of cost — this is the traditional domain of MR companies (i.e. consumer access) which no longer provides a barrier to entry Consulting companies – McKinseys of the world — are moving into the MR world, better able to present through storytelling, and better able to access companies through the C-Suite”- Pulled quote from OE

Following technology/innovation, there is an emphasis on how to properly use Data (20%) to Provide Value (15%) when so much secondary information is readily available. Suppliers have to continuously sell the value of primary research to clients; and client-side researchers have to convince their management that investment can provide better value out of newer, more in-depth research instead of just relying on all the data that already exist. Additionally, providing value could prove to be more purposeful as respondents identified Competition (12%) as a challenge due to online tools devaluing our services by making it easy for anyone to conduct research.

There is widespread access and usage of big data sources throughout the research industry, as well as, a number of solutions available to collect and analyze this data. The key element is how to integrate big data with “traditional” research, in order to provide a full understanding of consumers. Whether you are receiving or conducting research the results must invoke action to be valuable (business growth). As an insights provider the goal must not be to just collect relevant data, but to humanize the information so that clients/research buyers may use the results to achieve their business objective. More so, as automation, artificial intelligence, and the commoditization of research services continues to grow; competitive differentiation will stem from delivering useable report insights, or “now we know so we can” solutions.

“There is a lack of demonstrable results that provide significant impact on the businesses we support. We promise a lot in terms of rich insights, but I think the evidence of our success is limited or needs to be better publicized. Otherwise clients will continue to gravitate towards more low-cost / DIY solutions.”- Pulled quote from OE

As mentioned previously, the inability to provide consistent value has allowed big non-market research competitors to gain momentum in our market. Consultancies (Deloitte, McKinsey, IBM), DYI surveys (Survey Monkey) and big data suppliers (Google, Facebook) are all serious threats due to their household names and research capabilities. Marketing research suppliers must prove value for clients in the face of DIY and digitally available data or face the inevitable continued devaluation of their services. Researchers must counter the organizational belief that “big data” can provide all the insights businesses need to be successful, and that DIY survey templates are as good as professionally designed custom research.

“Traditional research (primary research, custom survey development, extensive high level analysis) is under pressure from faster, cheaper, easier approaches. The newer methods can produce reasonably good results which may appeal to many clients. Often these new methods cannot go into the depth and breadth of a custom survey, but may give a client half of what they need at a quarter of the cost and time. How do we educate clients to understand and appreciate the differences between quick and dirty research vs slower and more complete research?”- Pulled quote from OE

Digging in a bit deeper, the verbatim responses deliver a treasure trove of deeper context into how GRIT respondents feel about these issues. It’s worth pulling out a sample on a few key issues to highlight this.

The Big Data trough of disillusionment

In the Gartner hype cycle Big Data has definitely reached the trough of disillusionment stage within the market research industry with a wide range of challenges identified surrounding access, use and the analysis of new forms of data.

“The big data challenge – actually doing something with it!”

“No.1 challenge = Big data and how to use it”

Skills shortage

Many voice concerns that the market research industry lacks the skills to effectively compete.

“We are old fashioned, specifically in terms of what data, tools and methods are used. SPSS and simple cross-tabs and means comparison is widely used while the Analytics industry largely uses Python, R, and more sophisticated statistical/econometric/machine learning techniques.”

…and that our competitors in the world of consultancy and technology have better access to big data sources and are better skilled to interpret and market it which could potentially cut research companies out of the picture.

“Tech companies offering data and basic analysis , Google, Fb and other social media companies offering access and data, Consultancies , Automation, DIY survey providers and client internal capabilities in Analytics and Social Media monitoring – all offer clients a variety of consumer insight related products and services faster and at relatively lower prices”

A connection issue

The challenges most researchers voiced however was not surround the collection of data, access to data or the difficulties of analysing specific sources more how to connect the data they do have access to all together.

“Connecting different data sources, working with big data / identifying the relevant bits in big data”

“Disjointed data sources scattered across the organisation”

“Challenge = Dealing/synthesizing a multiplicity of data sources — primary/secondary, social listening, big data sources, etc.”

Questioning the value of big data

Some researcher are starting to question the real value of a lot of the new forms of data being generated and realising that in itself it is often of little value.

“A false belief that big data can provide all the insights marketing needs to be successful”

“Believing that big data changes behavior. The big data, machine learning, AI will all be helpful tools to the market research professional but all of it is meaningless without some thoughtful deliberation over what it means and how to use it. And none of it replaces valuable, rich insight into the human mind.”

GDPR

The final area of concern for a small but significant group of people in the industry is the impact of GDPR in 2018.

“GDPR and the extent that it does / does not affect Market research, and clients being concerned about DP when sharing sample information with us.”

The primary concern is about how it will impact on reducing sample supply

“GDPR – getting a large enough sample to be robust.”

And whether or not the industry is ready and prepared for the change.

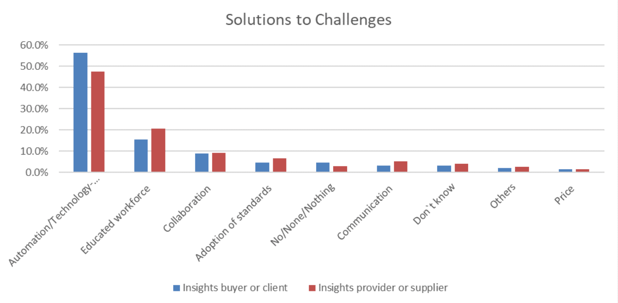

Solutions to Challenges

We were not content to simply provide a venue for the airing of concerns; we challenged GRIT respondents to propose solutions to the most serious issues they saw, and they did not disappoint.

As much as many respondents expressed concerns related to data and technology, even more saw technology as the potential panacea to these challenges, followed by more education and training as the very distant second option.

There is also recognition that the rise of new forms of data does provide clear opportunities for both new and old research solutions working together. There is a lot of talk about “getting the balance right” blending classical research methods to help make sense of new sources of data.

The industry has a double-edged sword mentality when it comes innovation however, and a deeper exploration of the verbatims sheds light on this seemingly contradictory perception.

Data Synthesis

You sense new range of synthesis methods emerging that blends classical qual and quant research to make sense of “big data” and bring it to life.

“We need to counter the assumption that big data provides sufficient information and insight without primary research about attitudes and motivations.”

“Professionals must find, through trial and error mostly, the right role for big data, quant and qual insights in their decision-making matrix.”

“Partnerships between those inside companies and market research firms to combine primary research with analytics and also bring external experience to projects.”

“Biggest near term opportunity is the effective combination of big data (rational) and qualitative research (emotional) to provide insights that have impact to the business”

“Combining Behavioural economics, Neuroscience, and AI to separate what consumers want people to think they do vs. what they actually do”

The looming threat of AI

Many market researchers fear the looming threat of AI, machine learning and worrying about how quickly we can get to grips with it, before our competitors do.

“AI and the adoption of technology that will replace the traditional syndicated research model”

“AI and IT industry becoming the competitor by out-pacing the market research industry’s innovative offerings and automating a way into eliminating the need for traditional researchers.”

AI the game changer…

But equally there are those that see the opportunities that AI and machine learning to be a real game changer for those in the research industry who can get ahead of the game.

“MR firms should embrace AI innovation in order to evolve”

The market research industry has always struggled to develop reliable predictive modelling techniques but machine learning could revolutionise this process.

“Predictive modelling – in the past models have been shaky at best but with the increasing amount of data points being generated & the developments in machine learning there is the opportunity to create far more accurate real time models”

The impact of DIY and self-serve solutions

There are lots of concerns about the impact of DIY solutions. There are worries that it is dumbing down research and that clients are starting to circumvent research firms as a result of easy access to do-it-yourself research tools.

“”do-it-yourselfers” using inexpensive, internal, packaged tools without the proper research knowledge to conduct research appropriately and to the correct respondent base”

“Clients who feel they can do it themselves with their own subscriptions to online survey platforms”

“DIY market research: people without research expertise thinking they don’t need to hire an expert to help them with research”

Data

Solutions to DIY encroachment

There were no clear “solutions” voices to the challenge of DIY other that recognising that it is up to market research firms to demonstrate their value and compete with it.

“Suppliers must continue to convince their clients of our value.”

“More communication about what a research professional brings to the table”

“Clients need education on the importance of the research value chain – research design, measurement design, analytics and insights. Tracking a handful of metrics via survey monkey is not research.”

“Solution = Innovation, working with our clients as a strategic partner to deliver rich insights, not easily gleaned from a more basic research study”

Perhaps the only way forward is to embrace it and add value…

“By accompanying the automation and DIY trend with the proper information, tools and expertise.”

DIY – clearly communicate the value added of expertise while reducing cost (offer modular work such as design only, design/analysis but no gathering, use of AI where applicable, etc.)

The impact of Automation

There are serious concerns from some quarters that the race to automation is commoditizing research.

“Automation lowering the perceived value of research will lead to the commoditization of our services.”

“Biggest challenge = Data Automation and the “dumbing down” of research to “cost per contact” and raise to pure commodity data.”

Whereas others see automation as the holy grail to enable our industry to become more competitive.

“Automation is the only solution.”

“More automation, more advanced analytical add ins in standard tools”

“Automation or semi-automation of analysis would greatly decrease the time it takes our firm to create a report.”

“Embrace the opportunities that come with digitalization: automation, faster insights, etc. rather than rejecting new technology / protecting the existing business.”

Keeping up with the pace of change

The general theme here is a concern about the research industries ability to adapt fast enough and keep up with the pace of change.

“Biggest challenge = Adapting to a fast-changing landscape of new and multiple competitors”

“Adapting to the changing needs of clients – ability to more flexible, quicker turnaround and ability to reach a broader target market”

“adapting to technology disruption”

A wild west of new techniques

There is a sense that with so many new shiny new techniques on offer, such a widening pool of new sources of data often untried and properly tested that the research industry is at a “wild west” stage of its evolution.

“sexy and cool implicit techniques that are easy to sell but are garbage and DIY – our standards as an industry have hit the ground floor and are heading to the basement. Cheap and quick are winning out over good.”

“Many of the new solutions coming out seem to be tech led rather than research led. This is apparent when speaking to companies, who have innovative solutions for research problems, but who do not really understand the research side of the business (eg how to analyse and interpret the information they are gathering). This means as a client I can use them in a field and tab type capacity, but if I want some serious consideration of how to adapt the tech for my research challenge or how to interpret the results and think of what they are showing in a more holistic way I will need to do this myself or hire a 3rd party”

Other researchers complain of clients not willing to try new methods and being stuck in their ways…

“Getting clients to try new research methods. Too many still cling to traditional methods when we know that consumers are increasingly less likely to participate in traditional surveys and focus groups. This is particularly true with FMCG marketers.”

“Challenge = Getting clients comfortable with the new technologies designed to leverage better insights – many are stuck with static tools and want any new solutions to replicate their static world”

We need to talk about Sample Quality

Issues surrounding accessing quality and representative sample is without doubt the single biggest individual challenge mentioned in the survey.

How to obtain a representative sample and lack of probability samples is a globally voiced problem.

“Survey research is getting harder to complete due to sample issues.”

“Continued decline in response rates across ALL modes and methodologies.”

General decline in the quality of sample with falling participation rates and accessing niche audiences another

“Respondent quality continues to be a big pain. when we dig into the respondents at an individual level from panel providers it is frustratingly low quality”

More and more professional respondents

“Data reliability, since real consumers are often not inclined to take part in researches. “Professional” respondents replace them quite often. Also, due to lack of consumers’ interest, it’s difficult to generate reliable, sincere and in-depth answers, – more and more efforts are required in order to find out something new.”

Tackling fraudulent respondents answering surveys is seen as a rising challenge.

“Fraudulent responses, whether generated by individual respondents for personal gain, or on a larger scale by sophisticated bots; challenge of getting quality respondents that meet client criteria to stay engaged with taking surveys over the long term.”

Research fatigue amongst respondents and the impact this was having on the quality of data was another commonly voiced challenge.

“Apathy from respondents, if we lose the sample we won’t be able to do the bread and butter of our job”

“We have to improve surveys. We continue to do too many long, tedious surveys. Clients are fooling themselves if they really think they are getting representative samples and quality data from these surveys.”

Solutions…

Encouraging shorter and more mobile compatible surveys was a fairly universal message

“better, shorter and more challenging surveys.”

“Shorter, more concise surveys Enhanced targeting to minimize # of questions and # of respondents screening out”

“Better engagement strategies for respondents, shorter surveys. The “do it yourself” platforms need to be accompanied by basic training in survey design, sampling methodology and statistics to lessen the diminishing of the profession by users that don’t understand the profession.”

Some feel that making surveys mobile compatible should be mandated and industry limits on the lengths of surveys.

“Need to cap survey length at 15 minutes and make sure all surveys are mobile friendly.”

Smarter use of data appending

Fresher sampling methods..

“More onsite recruitment in out of the box places like college campuses, festivals/events…basically boots on the ground instead of sending more and more emails “

Some ISO style standards that panel companies sign up to.

Recognising that more money needs to be fed back to panellist and that price pressure on panel supply was contributing to the problem.

“higher incentives, better quality checks/review of questionnaires”

“Price competitiveness – Too many firms going offshore charging almost nothing for research data collection”

Finding an industry solution…

Many though thought it was an industry problem that requires the industry to sit round the table and solve together.

“industry initiative with the involvement of all stakeholders”

“sample quality has to be addressed by all members of the research community.”

“Formation of deeper partnerships between buyer and supplier – more open dialogue between the two side.”

“The research vendors should be more transparent with some of the potential issues.”

“Clients perceive research sample as a commodity, and almost always buy on price; this reduces the margins of suppliers and thus also the amount of resources available to combat data quality issues.”

Solutions: New talent and re-organisation

Bringing in new talent into the research industry with fresh skills is commonly identified as a medium term solution. Other discussed ways in which research companies needed to be re-organise themselves.

“Our Division Insights team is actually undergoing a reorg to address new capabilities needed (i.e. Digital & E-Commerce roles) with specific training , but also lift up project management workload from lean team by outsourcing to extension team abroad. This will allow more time to focus on strategic initiatives and keep up with the ever-changing demands”

Organisations need to combine skills…

“Combining research skills (operations and project management), data analytics (statistical analysis and data mining) and business consulting (identify the issue, translate that to a research project and communicate and work with the client as a partner).”

Solutions: Reskilling and cross education

More education and training for the industry is viewed as vital for the industry to survive and transform itself.

“The marketing research profession is in danger of becoming a plug and play service. There is a lack of fundamental knowledge on data synthesis”

“Full service organizations making the shift to technology driven methods and insights generation. Too many organizations are wasting manual effort on processes that can be automated and both their speed of delivery and costs reflect it. Companies that won’t/can’t adapt will be driven out by technology-driven organizations who build technology to replace manual effort and bring on specialized talent to tell stories and curate data.”

It’s not just market researchers who need to learn, the new breed of data scientists need to better understand research. The lack of common sense from data analysist was viewed as a common challenge.

“Common sense knowledge of how to interpret data to understand the outcome. Too many times the “data scientist” really has no idea the applicability of the information to the real world. We need more people that can talk the data to people that are not necessarily market researchers.”

“Organizations should encourage cross-functional rotations into other areas of the their organizations that are impacted/request research. Thereby providing an increased understanding of the end user and how to apply to the business question/situation.”

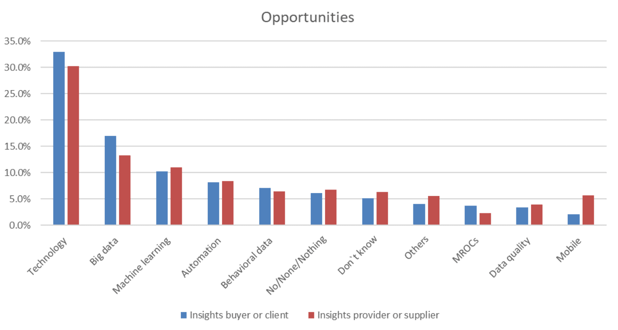

OPPORTUNITIES

The biggest near term opportunity facing the market research industry as indicated by respondents is Technology (31%). The main idea is that technology should be enabled to improve consumer data collection and compliment traditional research methods.

For primary research, opportunities exist to explore new ways of surveying with new platforms, new touch-points, and new approaches to engage the consumer. GRIT respondents feel that the market is currently saturated with traditional surveys and the influx of online DIY surveys. Leveraging technology to get insights where people are, where they make decisions, where they use products and services will be highly valuable moving forward. As project timelines continue to shrink, the ability to reach respondents in the moment for immediate feedback is very useful. One example includes using mobile devices and geo-fencing for in-the-moment research and retail experience surveys. Additionally, capitalizing on innovative research techniques through embracing more social media platforms and using text analytics to uncover themes was also noted. The big opportunity moving forward alongside technology is capturing unstated data through virtual reality, neurosciences, eye-tracking, and facial coding which in turn can be integrated with explicit data to give a full holistic view of the consumer.

“Technology utilization is the most obvious near-term opportunity. Online and mobile research are already present, but a very small fraction of qualitative research today. We need more researchers to be open to utilizing technology to pursue insights for their clients, versus the old school methods like focus groups that carry inherent bias.”- Pulled quote from OE

Technology isn’t going anywhere and is sure to only become more prominent. Instead of being skeptical of technology, the industry should embrace it and be on the front-end of its implementation to strengthen the value of our insights, and slow the tech and consultant companies of the world from encroaching into our market. The goal is to be a part of the technological revolution and not a competitor to it. This requires educating both suppliers and client researchers on the capabilities of technology and how it can be implemented to supplement and/or replace traditional (outdated) methodologies. In turn, the industry will get better at building bridges to the other disciplines that utilize consumer behavioral data and communicate its tangible value to clients. As we are becoming more innovative we need to better publicize the value of market research by demonstrating to clients why they should work with consumer research agencies and not entrust research to non-traditional research agencies.

Again a selection of verbatim responses shed light on these themes.

Machine learning and AI capabilities

The number one opportunity researchers identify surround the development of machine learning techniques to develop predictive modelling solutions.

“Artificial Intelligence to enable the harnessing of big data to derive insights which may have been previously impossible to spot”

“AI and predictive modeling, which, if properly used, may reduce the need for primary research”

The opportunities to do potentially do this in real time.

“AI around analytics and MR to predict behavior online in real-time”

Pushing forward with Automation

Increasing levels of automation is seen as the second most important opportunity for the industry to improve its operational efficiency and become more competitive.

“Automation of data gathering, analysis, reporting and alerts”

“Automation, as companies collect more and more data we need systems which can sift through this data as the size of research teams become more and more unmanageable”

Becoming the why

Using classical old skool research methods to help better understand big data is seen as a growing opportunity.

“Becoming the “why” answer to big data. The big data/analytics folks tell you something is occurring behaviorally, but they rarely can tell you why without talking to people exhibiting the behavior.”

Diversifying data collection methods

Proactively diversify the type of data collection methods being use to take advantage of new techniques is seen as an opportunity by some researchers

“Adopt a greater range of data collection techniques.”

“continued evolution to holistic use of data from various sources, as well as development of new methodologies in part driven by AI”

Total MR

Exploring research opportunities outside the marketing department is seen as a growth area

“Applying insights across the entire organization, besides just marketing (e.g., advertising, branding). Doing so will help market research as a discipline grow and become better understood (and respected) within organizations.”

Talking research

In home help devices the like of Alexa many people see as opening up new ways to conduct research in a more spontaneous and natural way.

“Integrating new technology into ethnographies, i.e. respondents giving permission for Alexa to follow you for a day”

Geo-targeting & VR

The ability to conduct more precisely targeted pieces of research based on mobile phone location is seen as an undeveloped opportunity. There are also are several mentions of the possibilities surrounding virtual reality but both of these ideas are rather lacking in specifics.

“Immersions Virtual reality Online following System 1”

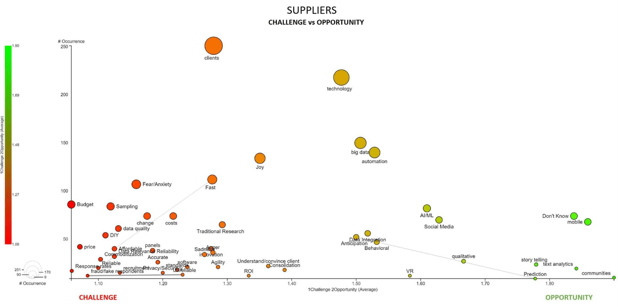

The Main Story

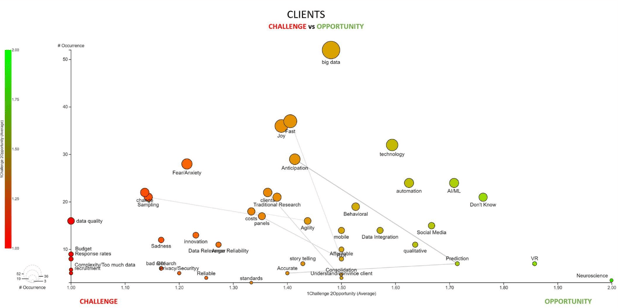

GRIT respondents are clear that the industry is under immense pressure to change, and many of the issues that are threats (AI, automation, Big Data, training and education, sample quality) are also potential solutions. This is most clearly illustrated using text analytics to analyse the combination of emotional valence for each topic, it’s plot as numbers of mentions as either a challenge and/or an opportunity, and mentions by clients and suppliers:

The difference seems to be one of pragmatism vs. purity; how do we enhance and advance the role of insights and the value it delivers when so many new tools, approaches, and business models are based on driving speed, cost, and quality via technology? This tension won’t be solved any time soon, but the good news is that optimism seems to be more prevalent than fear, so we think the industry will navigate these changes just fine in the long run.